The following is the balance sheet of associated enterprises limited as december 31 2012. Show journal entries in the books of x ltd. Along with this the company further decided to utilise the balance of share premium account to issue fully paid up bonus shares in the ratio of one equity share for every five equity shares held.

Rs 100 rs 90. The amount of discount is rs 10 per share i e. 90 each the shares are said to be issued at discount.

For example if a company issues its shares of rs 100 each at rs. When the issue price of share is less than the face value shares are said to have been issued at discount. Journal entries issue of shares at discount.

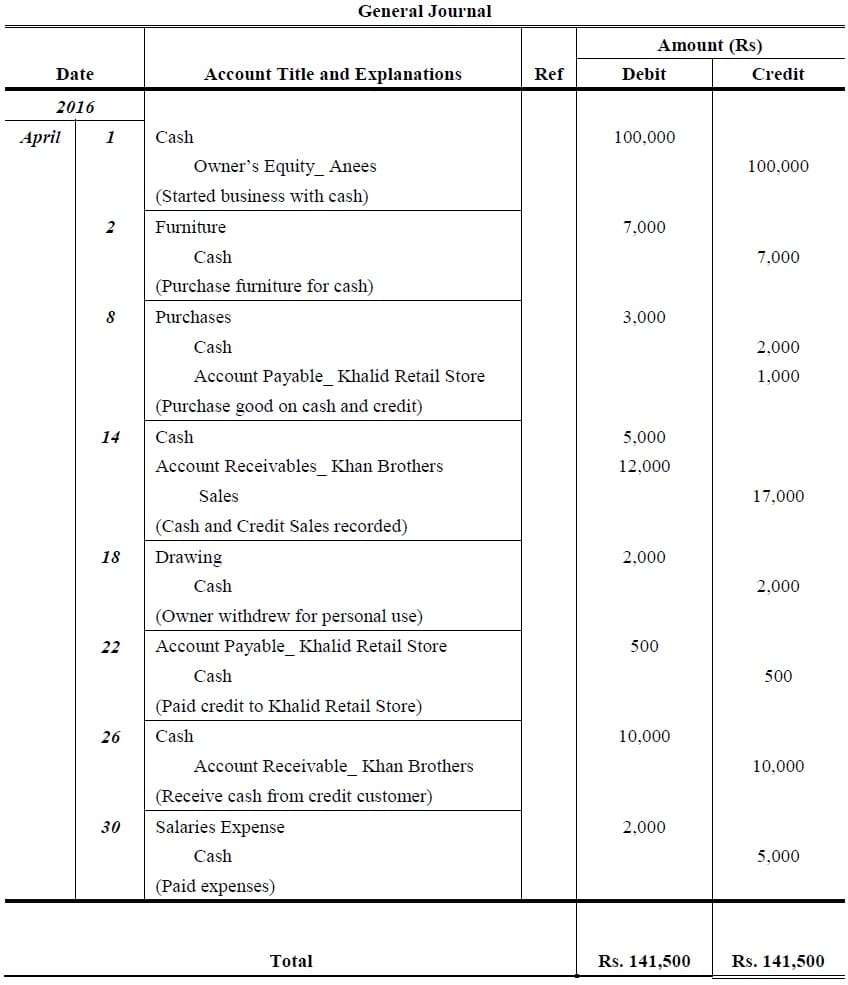

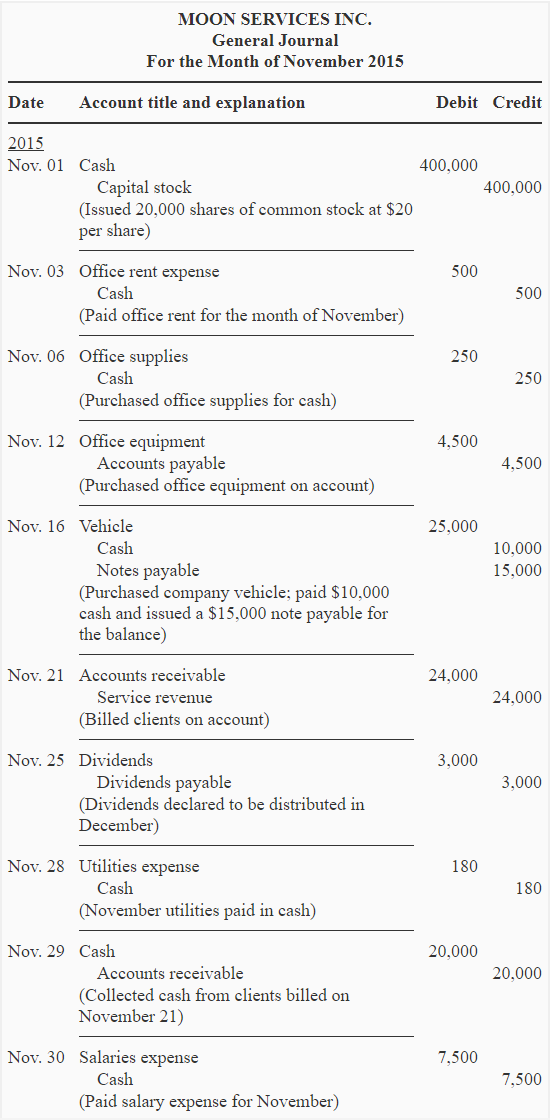

Each journal entry is also accompanied by the transaction date title and description of the event. Traditional journal entry format dictates that debited accounts are listed before credited accounts. Journal entries use debits and credits to record the changes of the accounting equation in the general journal.

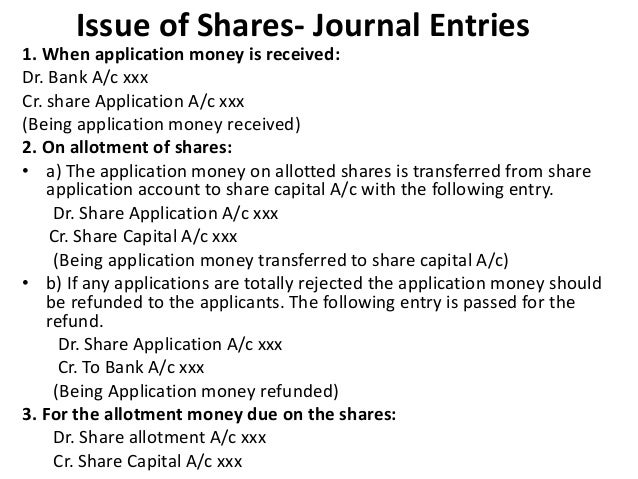

For this the company will pass the following entry. On the allotment of share the allotment money becomes due to the company. Learn about the correct procedure of journal entries for issue of shares.

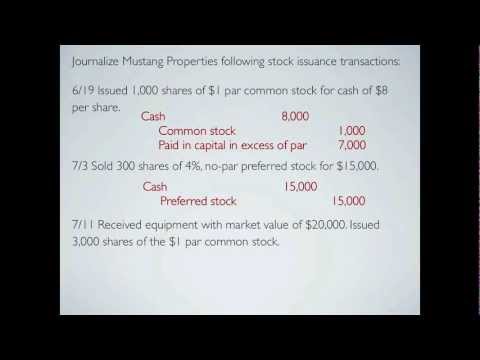

Journal entries examples for issue of shares. Make journal entries to record the issue of shares. All money was duly received.

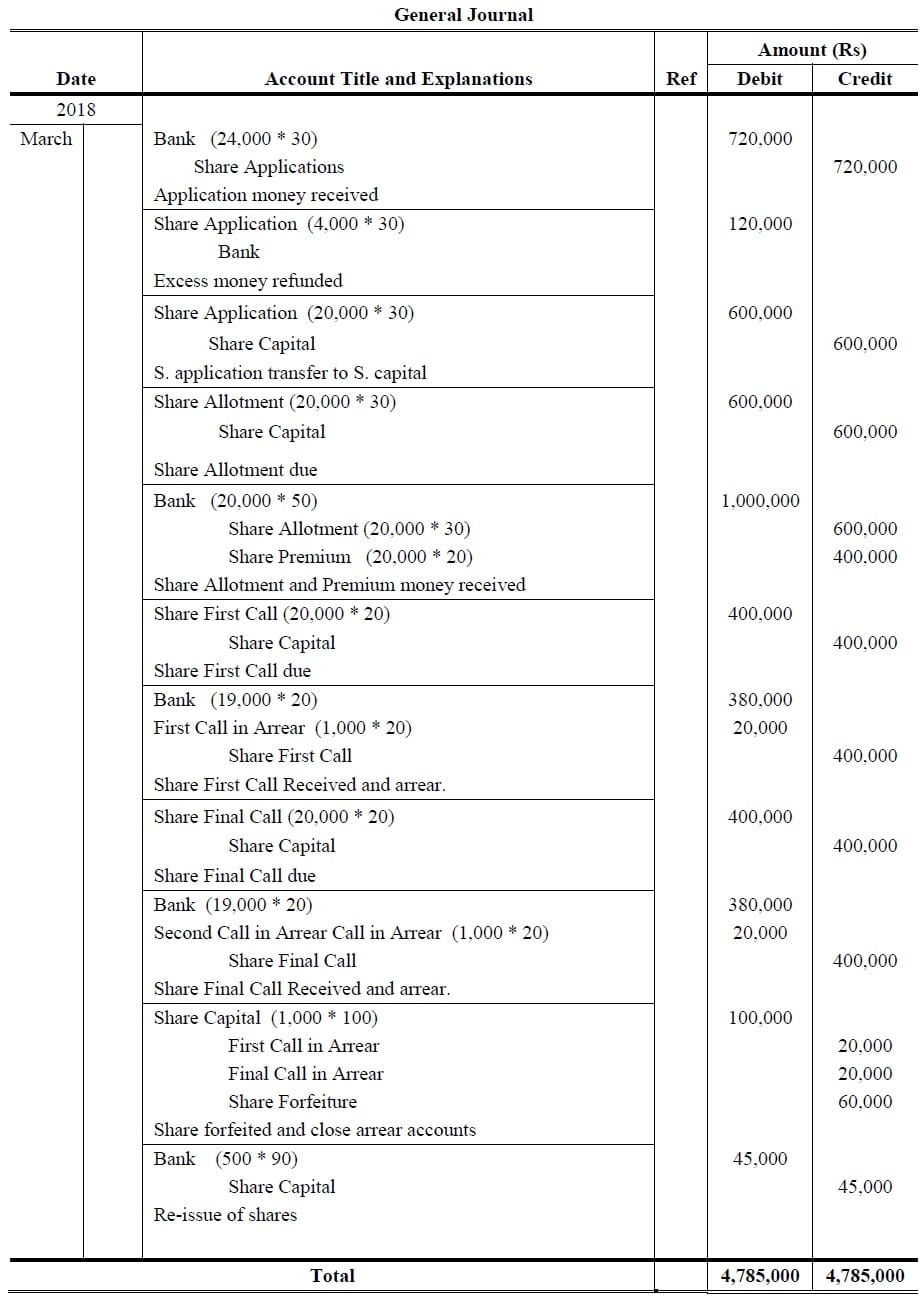

20 on the final call.

Issue of shares journal entries format. A company may issue shares for consideration other than cash. It may for example purchase some fixed assets for which it may make payment in the form of shares. Or it may take over a running business and the consideration for the business may be discharged by the company fully or partly in the form of its own shares. Entries will be as follows.

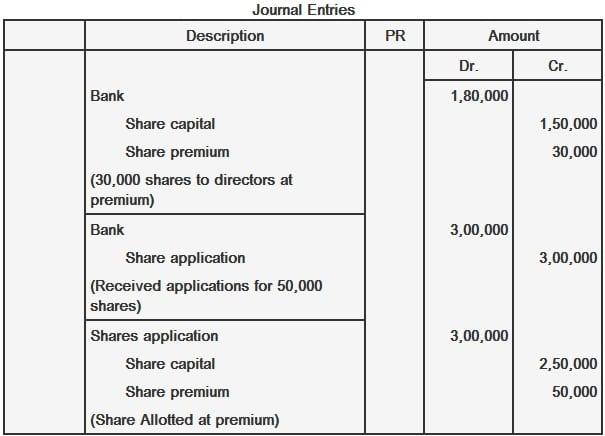

Issue of shares at premium. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share. In other words the premium is the amount over and above the face value of a share. Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium.

There are various ways or prices at which a company issues its shares like at par at a premium and at discount. The issue of shares at a discount means the issue of the shares at a price less than the face value of the share. For example if a company issues share of rs 100 at rs 90 then rs 10 i e. Rs 100 90 is the amount of discount.

Such issues of shares have been clearly shown in balance sheet and distinguish such shares from shares issued for cash. The journal entry is. When the settlement is made by issue of shares of fully paid shares such shares are known as shares issued for consideration other than cash. Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share.

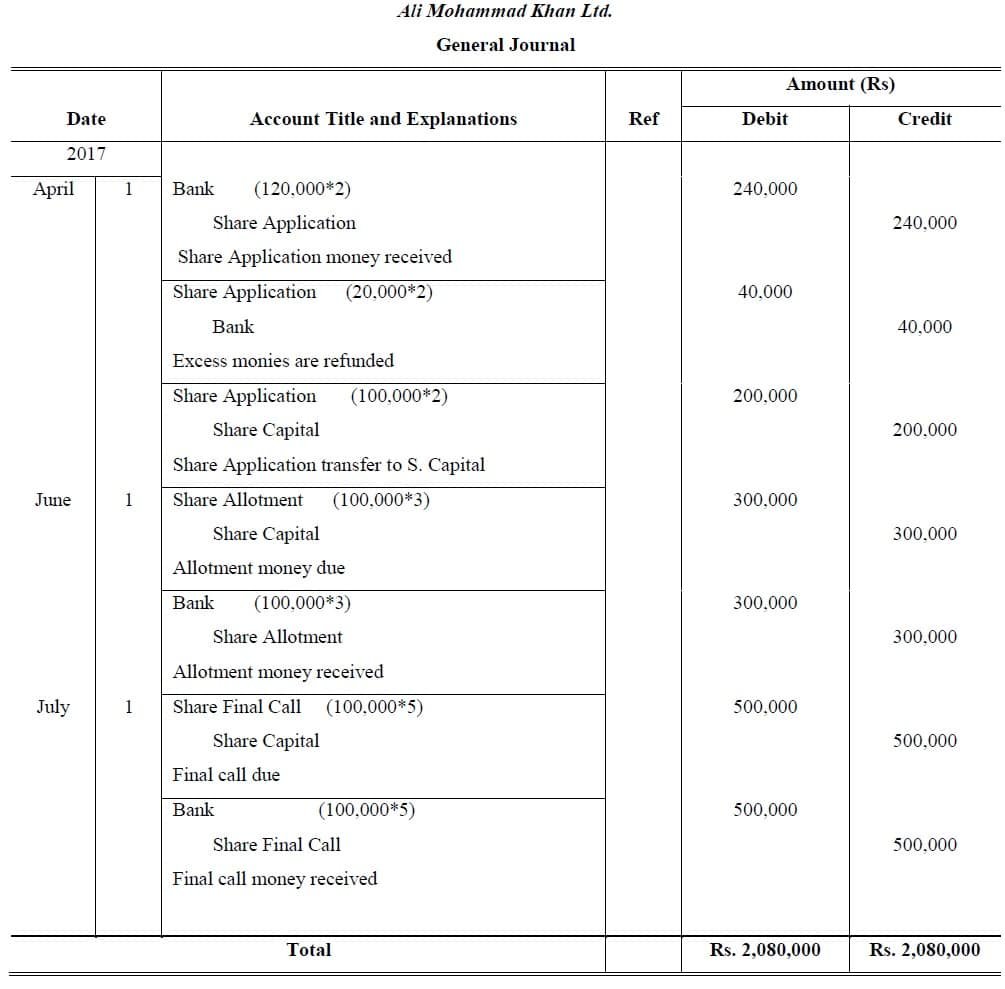

As per the terms of the issue 1 25 per share had been received by the company on 1 january 20x4 while the remaining amount was received in full on 30 june 20x4. State the journal entries required to account for the. Its capital is divided into 8 000 equity shares of rs. The company issued 6 000 shares to the public payable rs.

30 per share on application rs. 20 per share on allotment rs. 30 per share on first call and the balance rs.

30 per share on first call and the balance rs. 20 per share on allotment rs. 30 per share on application rs.

The company issued 6 000 shares to the public payable rs. Its capital is divided into 8 000 equity shares of rs. State the journal entries required to account for the.

As per the terms of the issue 1 25 per share had been received by the company on 1 january 20x4 while the remaining amount was received in full on 30 june 20x4. Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share. When the settlement is made by issue of shares of fully paid shares such shares are known as shares issued for consideration other than cash.

The journal entry is. Such issues of shares have been clearly shown in balance sheet and distinguish such shares from shares issued for cash. Rs 100 90 is the amount of discount.

For example if a company issues share of rs 100 at rs 90 then rs 10 i e. The issue of shares at a discount means the issue of the shares at a price less than the face value of the share. There are various ways or prices at which a company issues its shares like at par at a premium and at discount.

Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium. In other words the premium is the amount over and above the face value of a share. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share.

Issue of shares at premium. Entries will be as follows. Or it may take over a running business and the consideration for the business may be discharged by the company fully or partly in the form of its own shares.

It may for example purchase some fixed assets for which it may make payment in the form of shares. A company may issue shares for consideration other than cash.