Following journal entries are required to account for a bonus issue. Bonus issue is a simple reclassification of reserves which causes an increase in the share capital of the company on one hand and an equal decrease in other reserves. Such issues of shares have been clearly shown in balance sheet.

Many times it is seen that shares have been allotted to persons or firms from whom assets have been purchased. In this article we will discuss about the journal entries required for the issue of shares explained with the help of suitable illustrations. Being the share allotment money due on share rs per share as per resolution dated 4 on receipt of allotment money the entry is.

To share capital account. For this the company will pass the following entry. 3 on the allotment of share the allotment money becomes due to the company.

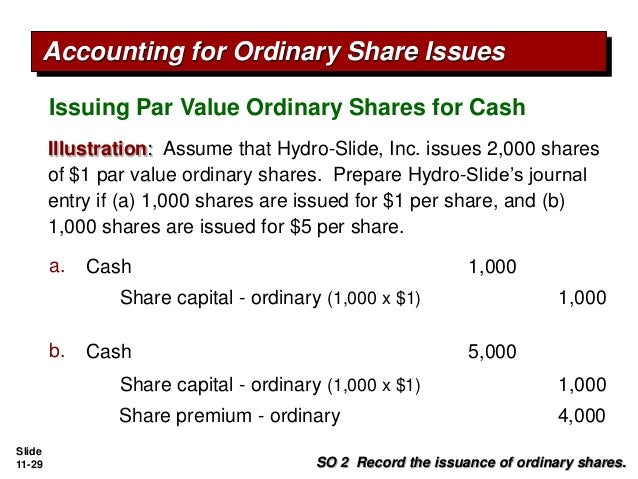

Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium. In other words the premium is the amount over and above the face value of a share. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share.

Issue of shares at premium. State the journal entries required to account for the. As per the terms of the issue 1 25 per share had been received by the company on 1 january 20x4 while the remaining amount was received in full on 30 june 20x4.

Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share. However there is only one exception that is the existing share holders know in advance the number of shares to which they will be entitled. Accounting entries in the books of company for right issue are the same as those required for a new issue of shares to the public.

Right shares means the shares where the existing shareholders have the first right to subscribe the shares.

Right issue of shares journal entry. Accounting entries on issue of right shares and bonus shares. Issue of right shares. Section 81 of the companies act requires that a public limited company whenever it proposes to increase its subscribed capital after the expiry of two years from the date of its incorporation or after the expiry of one year from the date of allotment of shares in that company made for the first time after. Rights issue is one of the way by which a company can raise equity share capital among the various types of equity share capital sources available.

These are slightly different from the standard issue of shares.

These are slightly different from the standard issue of shares. Rights issue is one of the way by which a company can raise equity share capital among the various types of equity share capital sources available. Section 81 of the companies act requires that a public limited company whenever it proposes to increase its subscribed capital after the expiry of two years from the date of its incorporation or after the expiry of one year from the date of allotment of shares in that company made for the first time after.

Issue of right shares. Accounting entries on issue of right shares and bonus shares.