Investment income as far as the valuation of these bonus shares is concerned you should take the fair market value closing rate of the date on which you received your bonus shares. In case of bonus shares received the following entry would be recorded. State the journal entries required to account for the.

As per the terms of the issue 1 25 per share had been received by the company on 1 january 20x4 while the remaining amount was received in full on 30 june 20x4. Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share. A shareholder with 1 000 shares receives 1 500 bonus shares 1000 x 3 2.

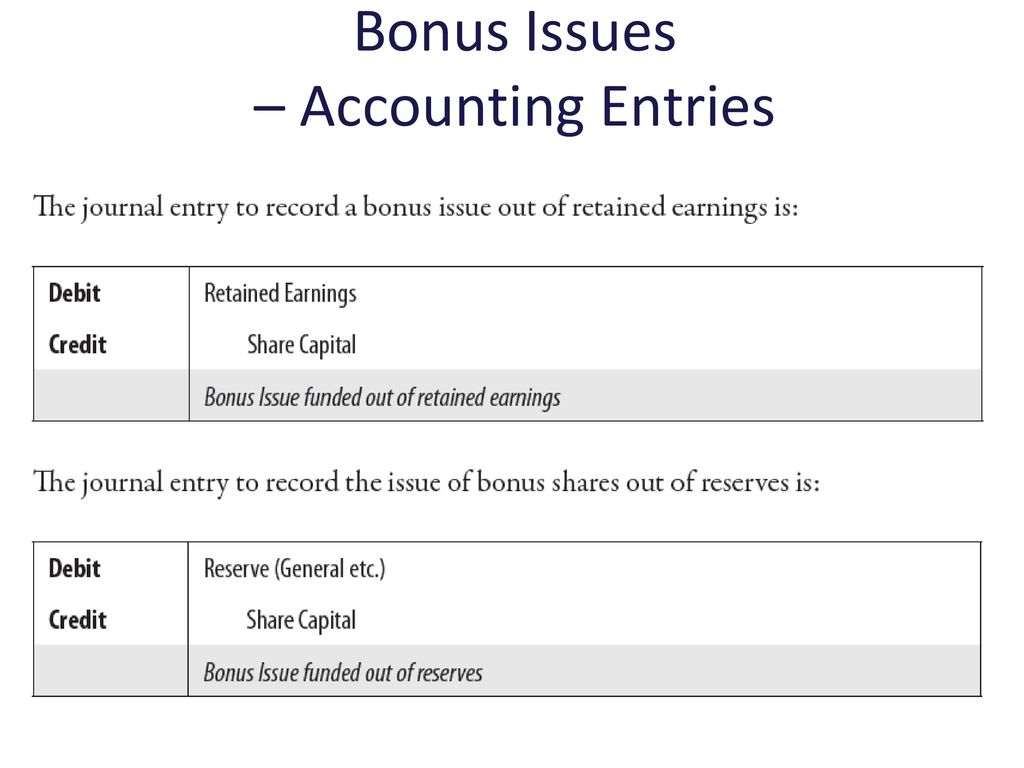

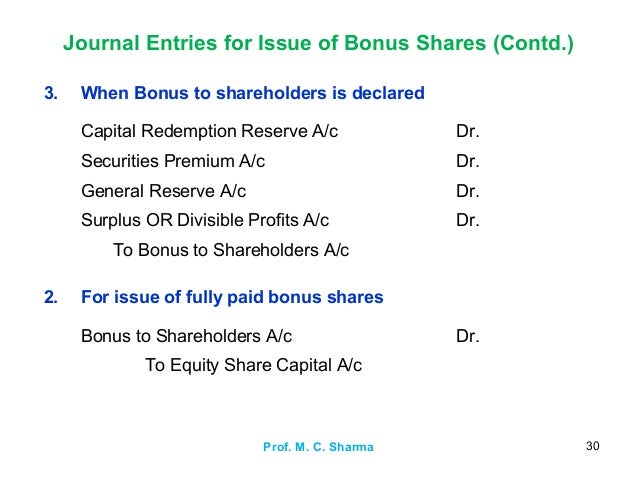

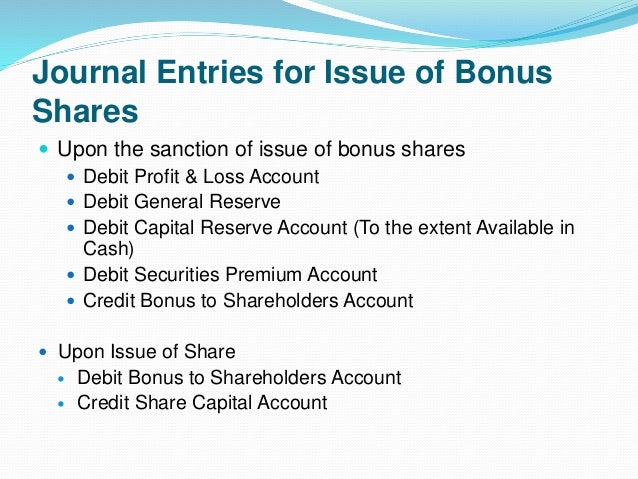

For example a three for two bonus issue entitles each shareholder three shares for every two they hold before the issue. Journal entries a 1 upon the sanction of an issue of bonus shares a debit profit loss account debit general reserve account. Substantial reserves in comparison to their paid up capital issue bonus shares to capitalize the reserves for which the certain norms conditions and criteria may be followed and fulfilled.

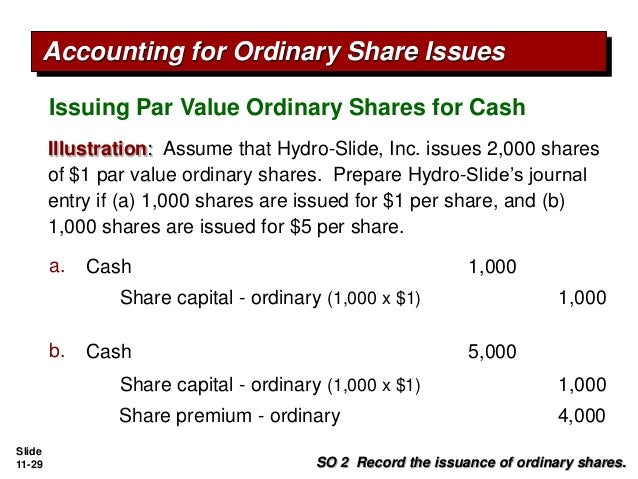

Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium. In other words the premium is the amount over and above the face value of a share. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share.

Issue of shares at premium. The accounting entry for the issuance of bonus shares would be. The issue of bonus shares in payment of dividend is called capitalization of un distributed profit.

In this way shareholders will get additional shares without making any further payment. The shares thus issued are known as bonus shares. So his total holding would be 1 00 000 50 000 1 50 000 of which 50 000 shares are allotted free.

Hence if a shareholder has 1 00 000 shares in his account the bonus 1 00 000 1 2 50 000.

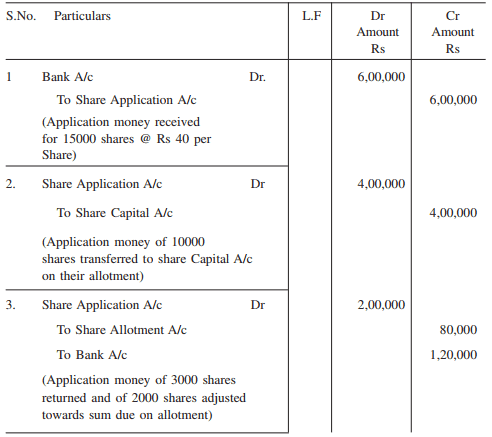

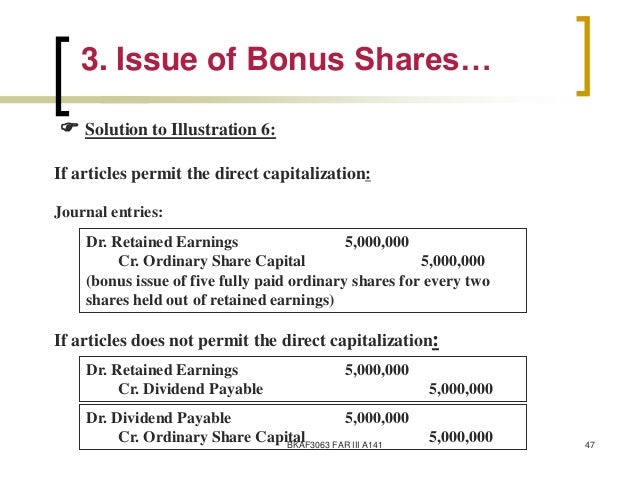

Journal entry for issue of bonus shares. Ii the issue of bonus shares to the equity shareholders in the ratio of one share for every four shares held by them. You are required to pass necessary journal entries. Since fresh issue is made to the extent of rs. 6 00 000 12 00 000 6 00 000 has been transferred to capital redemption reserve account.

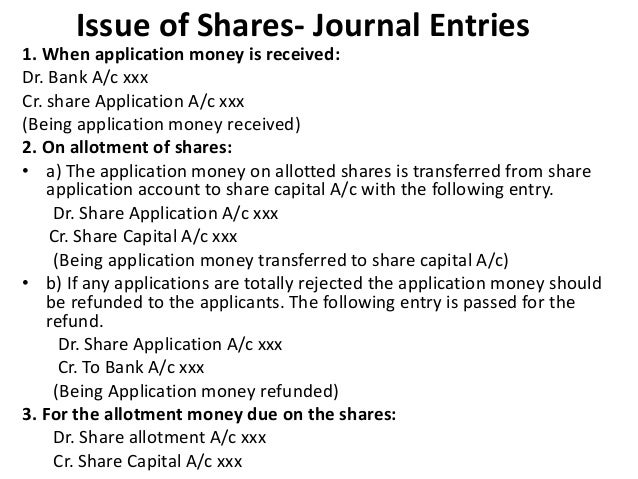

Bonus issue is a simple reclassification of reserves which causes an increase in the share capital of the company on one hand and an equal decrease in other reserves. Following journal entries are required to account for a bonus issue. Accounting entries on issue of right shares and bonus shares. Issue of right shares.

Section 81 of the companies act requires that a public limited company whenever it proposes to increase its subscribed capital after the expiry of two years from the date of its incorporation or after the expiry of one year from the date of allotment of shares in that company made for the first time after. Bonus shares issue journal entries. The company announces bonus shares in the form of a ratio i e 1 2 this means every shareholder who has 2 shares.

The company announces bonus shares in the form of a ratio i e 1 2 this means every shareholder who has 2 shares. Bonus shares issue journal entries. Section 81 of the companies act requires that a public limited company whenever it proposes to increase its subscribed capital after the expiry of two years from the date of its incorporation or after the expiry of one year from the date of allotment of shares in that company made for the first time after.

Issue of right shares. Accounting entries on issue of right shares and bonus shares. Following journal entries are required to account for a bonus issue.

Bonus issue is a simple reclassification of reserves which causes an increase in the share capital of the company on one hand and an equal decrease in other reserves. 6 00 000 12 00 000 6 00 000 has been transferred to capital redemption reserve account. Since fresh issue is made to the extent of rs.

You are required to pass necessary journal entries. Ii the issue of bonus shares to the equity shareholders in the ratio of one share for every four shares held by them.