This contrasts with issuing par value shares or shares with a stated value. Since the company may issue shares at different times and at differing amounts its credits to the capital stock account are not uniform amounts per share. Journal entries to issue stock.

In fact majority of the additional money which he paid is the share premium my question is what additional journal entry do i need to process for the shares premium so it can reconcile his loan account. Due to this his overall loan account shows a credit balance payable by the company. Dr bank cr shareholder loan cr share premium.

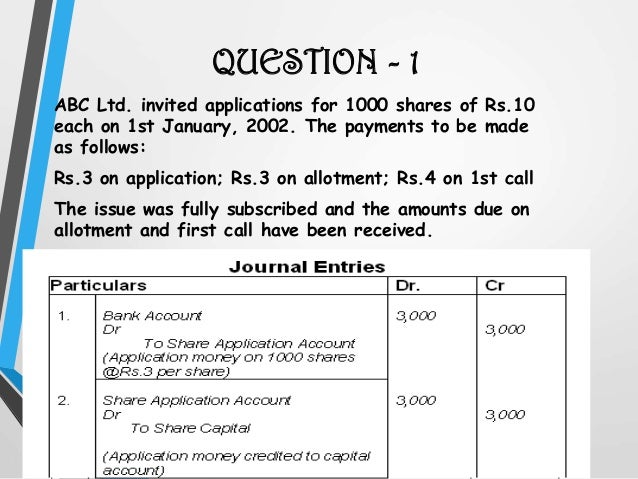

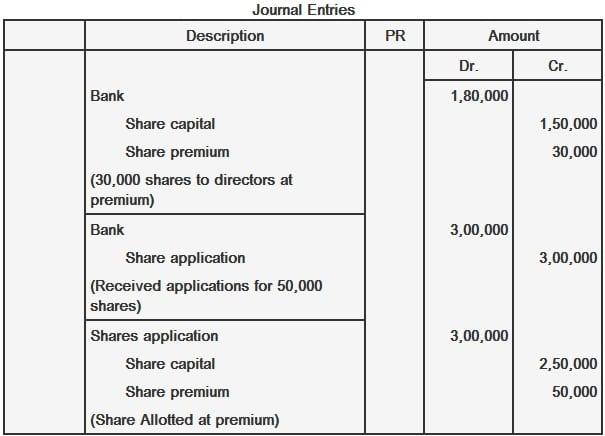

If the securities premium is collected on application and the company has taken decision about the allotment of shares the following journal entry is made. A securities premium collected with share application money. Following is the accounting treatment of premium on issue of shares.

Accounting treatment of premium on issue of shares. Or it may take over a. It may for example purchase some fixed assets for which it may make payment in the form of shares.

A company may issue shares for consideration other than cash. In this article we will discuss about the journal entries on issue of shares for consideration other than cash. Promoters bring the company into existence.

These shares may either be issued at par or at a premium or at a discount. When the settlement is made by issue of shares of fully paid shares such shares are known as shares issued for consideration other than cash. If shares are issued to the directors or underwriters at a premium.

Journal entries for issuance of shares at a premium.

Issue of shares at premium journal entries. Issue of shares at premium. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share. In other words the premium is the amount over and above the face value of a share. Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium.

Accounting entries regarding issue of shares at par. A company may issue shares at their face value or at a price other than the face value. When shares are issued at a price equal to their face value it is termed as shares issued at par. When issue price of a share is more than its face value it is known as shares issued at a premium.

There are various ways or prices at which a company issues its shares like at par at a premium and at discount. The issue of shares at a discount means the issue of the shares at a price less than the face value of the share. For example if a company issues share of rs 100 at rs 90 then rs 10 i e. Rs 100 90 is the amount of discount.

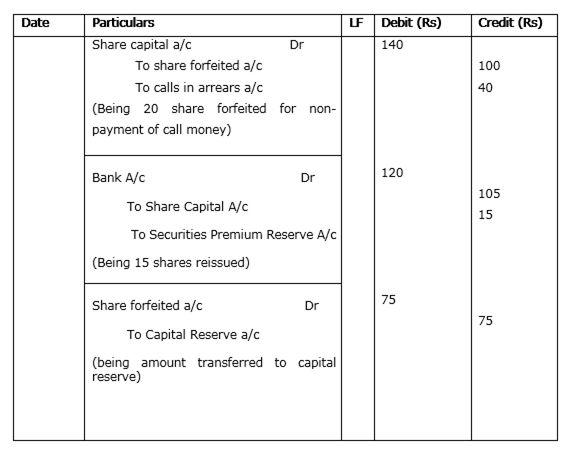

The total amount recognized in the share capital account is 1 million which equates to the nominal value of the issued shares i e. 1 per share whereas the cash proceeds over and above the nominal value amounting 500 000 i e. 0 5 per share has been credited to the share premium account. The premium received on issue shares must not be mixed with the share capital but must be credited to separate account called share premium account and shown as separate item on the liability side of the balance sheet.

The premium received on issue shares must not be mixed with the share capital but must be credited to separate account called share premium account and shown as separate item on the liability side of the balance sheet. 0 5 per share has been credited to the share premium account. 1 per share whereas the cash proceeds over and above the nominal value amounting 500 000 i e.

The total amount recognized in the share capital account is 1 million which equates to the nominal value of the issued shares i e. Rs 100 90 is the amount of discount. For example if a company issues share of rs 100 at rs 90 then rs 10 i e.

The issue of shares at a discount means the issue of the shares at a price less than the face value of the share. There are various ways or prices at which a company issues its shares like at par at a premium and at discount. When issue price of a share is more than its face value it is known as shares issued at a premium.

When shares are issued at a price equal to their face value it is termed as shares issued at par. A company may issue shares at their face value or at a price other than the face value. Accounting entries regarding issue of shares at par.

Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium. In other words the premium is the amount over and above the face value of a share. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share.

Issue of shares at premium.