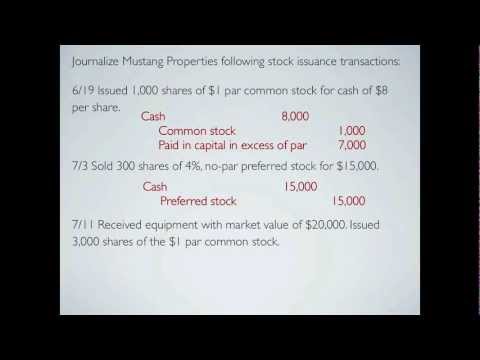

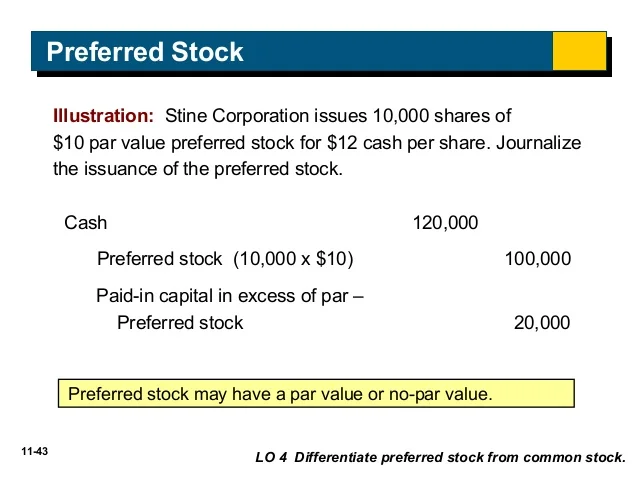

The transaction is journalized as follows. They carry dividend of 3 per share. Company a issued 100 000 shares of preferred stock of 30 par value against 1 000 000 in cash and 2 000 000 worth of property plant and equipment.

Journal entry for issuance of preferred stock. Redeemable preference share capital account dr. At that time we will pass following journal entry.

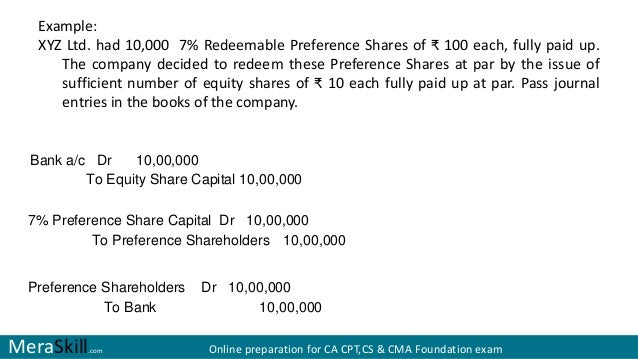

When preference shares are due on the maturity date with its premium amount. Following entries are passed while redemption of preference shares. Although shares may be equity shares or preference shares but if the term shares is used it means equity shares relevant accounts.

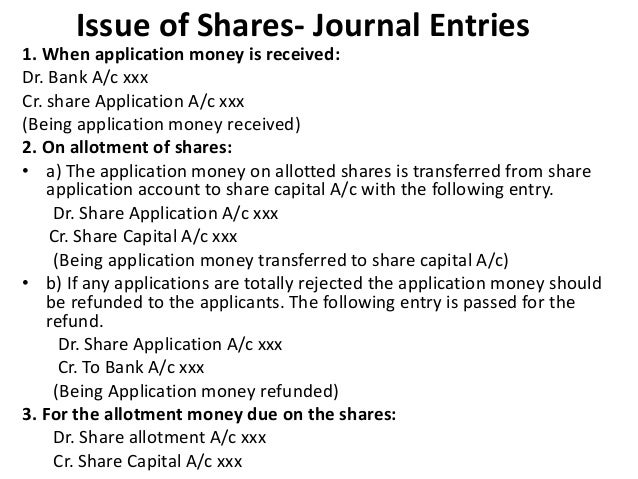

Fashion fabrics ltd journal entries note. Make journal entries and prepare relevant accounts in the books of company. Rs 5 per share on call.

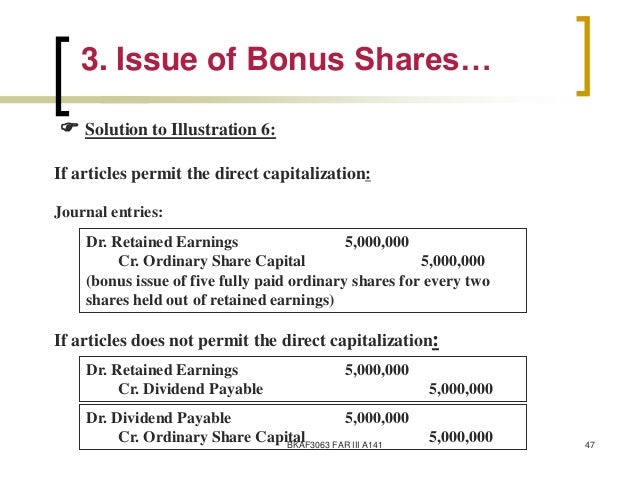

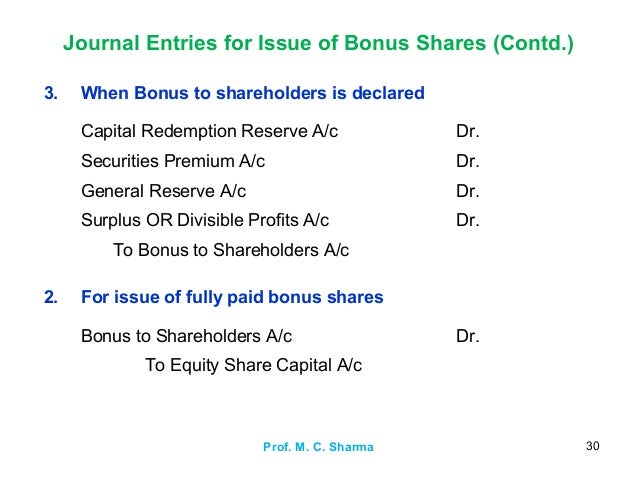

When the settlement is made by issue of shares of fully paid shares such shares are known as shares issued for consideration other than cash. The journal entry is. Such issues of shares have been clearly shown in balance sheet and distinguish such shares from shares issued for cash.

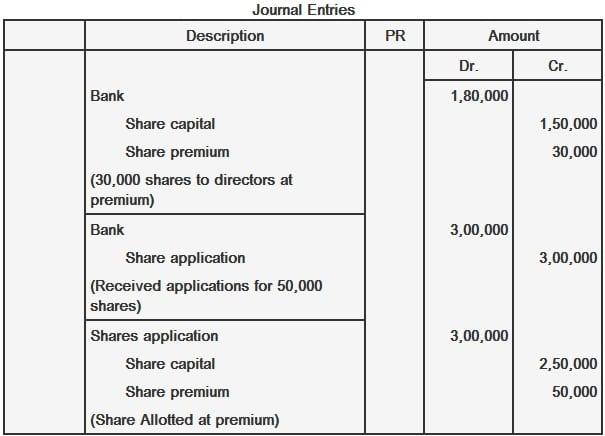

Applications were received for 2 000 shares on 1st april 2018. Harry limited with an authorized capital of 2 00 000 divided into 4 000 shares of 50 each has taken necessary steps to issue 3 000 shares at a discount of 10 out of these 500 shares were issued to directors on 25th march 2018 and 2 500 shares to the general public. State the journal entries required to account for the.

As per the terms of the issue 1 25 per share had been received by the company on 1 january 20x4 while the remaining amount was received in full on 30 june 20x4.

Issue of preference shares journal entries. The issue of preference share. If company liquefies the owners of preference shares will be the first one to get their money back after the company has paid its debt. Preference shares also have a right to participate in excess profits left after paying the equity shareholders. Issue of shares at premium.

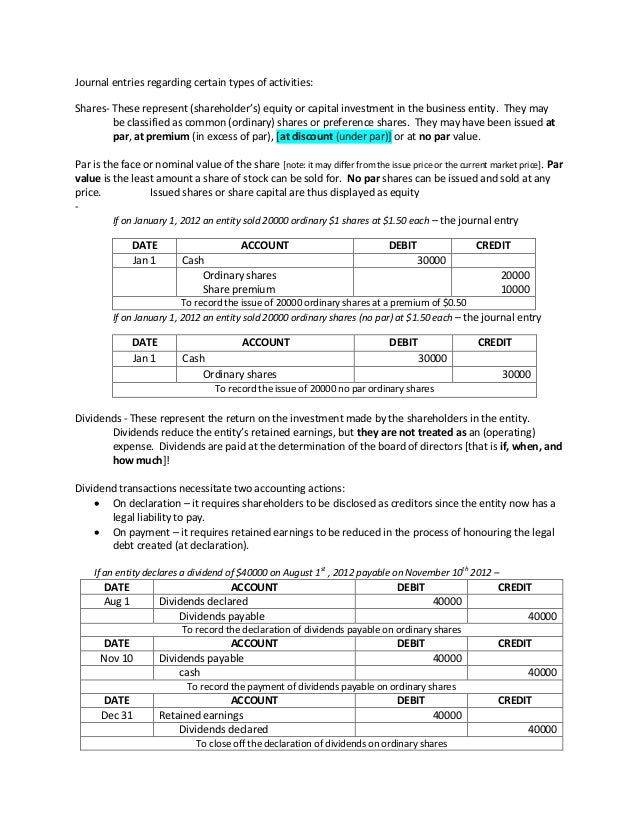

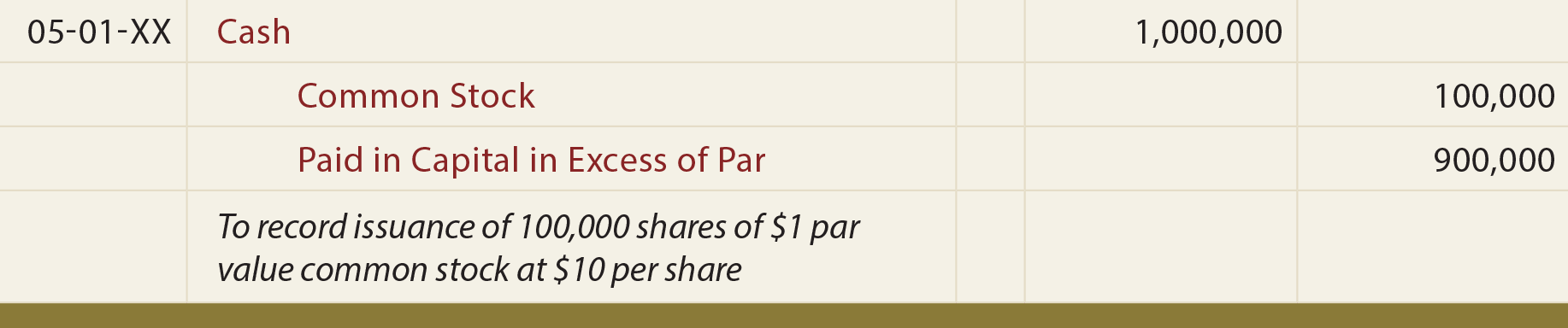

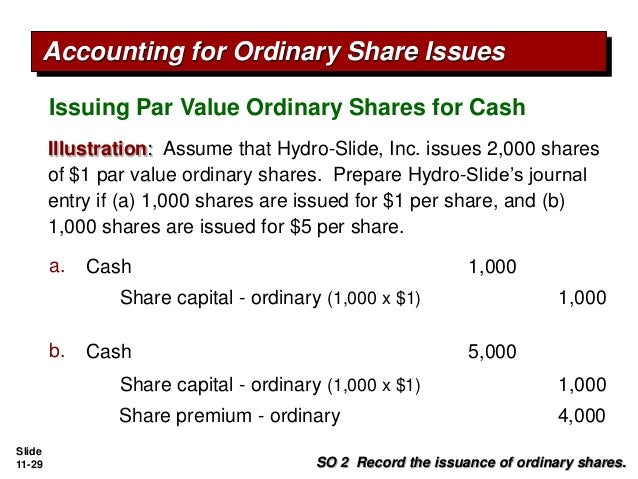

The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share. In other words the premium is the amount over and above the face value of a share. Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium. Accounting entries regarding issue of shares at par.

A company may issue shares at their face value or at a price other than the face value. When shares are issued at a price equal to their face value it is termed as shares issued at par. When issue price of a share is more than its face value it is known as shares issued at a premium. The issue was fully subscribed and paid for on april 15 2012 the company redeemed all the preference shares.

Pass necessary journal entries to record the transactions. Decided to redeem their preference shares as on march 31 2012 on which date their position was as under. Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share.

Abc plc issued 1 million ordinary shares on 1 january 20x4 having face value of 1 each at an issue price of 1 5 per share. Decided to redeem their preference shares as on march 31 2012 on which date their position was as under. Pass necessary journal entries to record the transactions.

The issue was fully subscribed and paid for on april 15 2012 the company redeemed all the preference shares. When issue price of a share is more than its face value it is known as shares issued at a premium. When shares are issued at a price equal to their face value it is termed as shares issued at par.

A company may issue shares at their face value or at a price other than the face value. Accounting entries regarding issue of shares at par. Usually the companies that are financially strong well managed and have a good reputation in the market issue their shares at a premium.

In other words the premium is the amount over and above the face value of a share. The issue of shares at premium refers to the issue of shares at a price higher than the face value of the share. Issue of shares at premium.

Preference shares also have a right to participate in excess profits left after paying the equity shareholders. If company liquefies the owners of preference shares will be the first one to get their money back after the company has paid its debt. The issue of preference share.