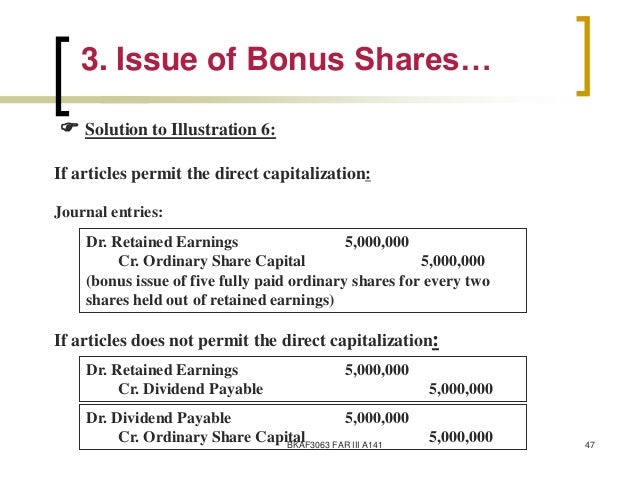

Journal entries a 1 upon the sanction of an issue of bonus shares a debit profit loss account. A bonus issue or scrip issue is a stock split in which a company issues new shares without charge in order to bring its issued capital in line with its employed. If the directors.

The undistributed profit of the company or corporation is transferred to profit and loss appropriation account or retained earning. Explanation and journal entries. Explanation and journal entries.

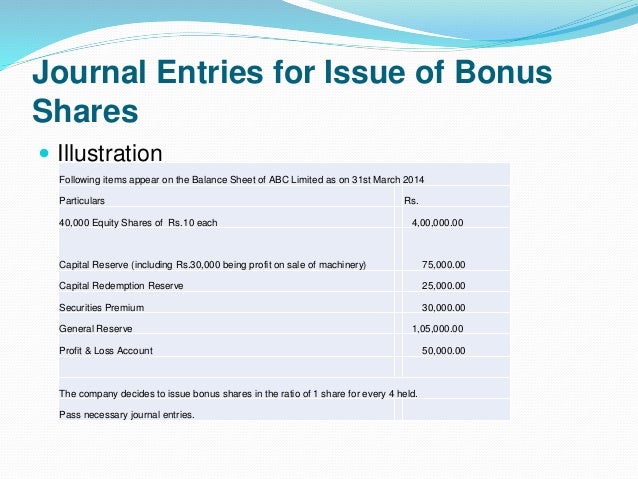

November 16 2018 february 12 2018 by rashidjaved. Issue of bonus shares. Bonus shares are issued from the reserves of a company.

When bonus shares are issued the accounting entry is different from normal issue of shares. For example 1 bonus share may be issued for every 3 shares a shareholder possesses. These issues are given to shareholders free of charge based on the existing number of the shares they hold.

So his total holding would be 1 00 000 50 000 1 50 000 of which 50 000 shares are allotted free. Hence if a shareholder has 1 00 000 shares in his account the bonus 1 00 000 1 2 50 000. The company announces bonus shares in the form of a ratio i e 1 2 this means every shareholder who has 2 shares.

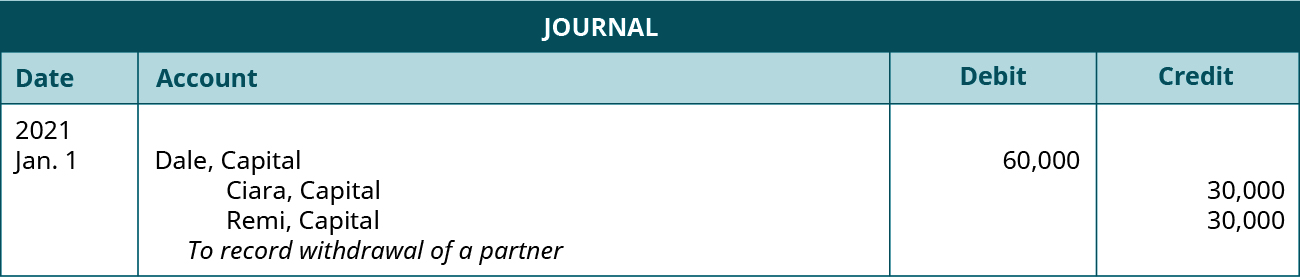

Bonus shares issue journal entries. You are required to pass necessary journal entries. And ii the issue of bonus shares to the equity shareholders in the ratio of one share for every four shares held by them.

20 per share on equity shares for the purpose of making the said equity shares fully paid.

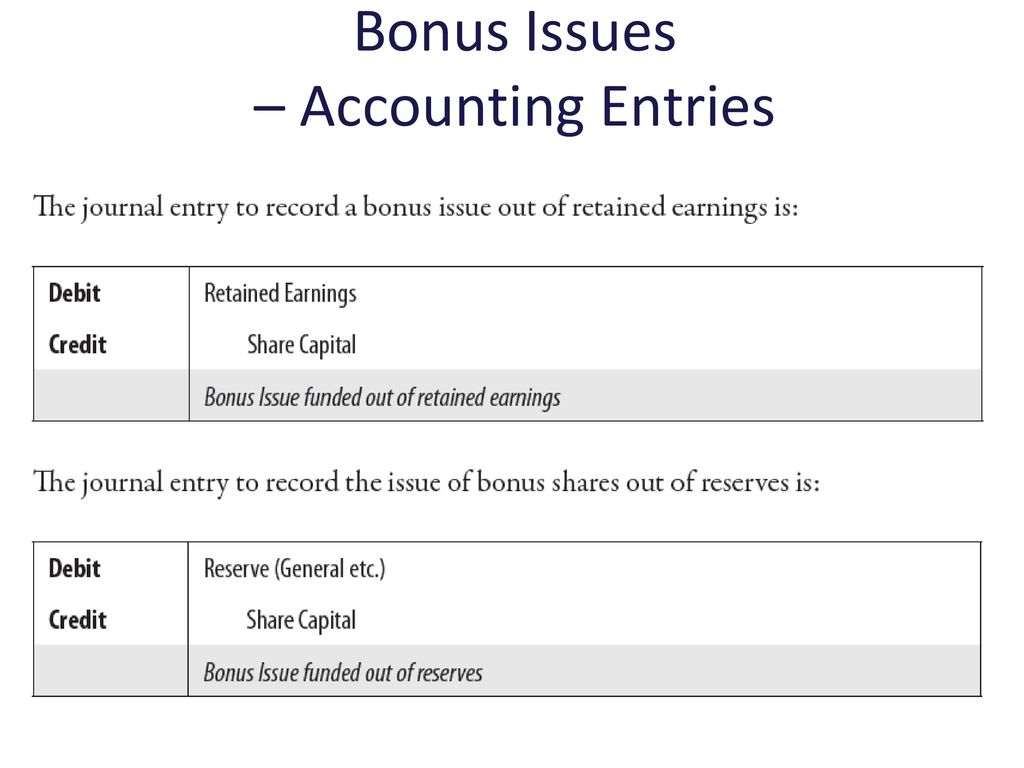

Bonus issue journal entry. Bonus issue is a simple reclassification of reserves which causes an increase in the share capital of the company on one hand and an equal decrease in other reserves. Following journal entries are required to account for a bonus issue. The company declared bonus out of its reserve fund of rs. 12 00 000 and this bonus is to be paid by issue of fully paid equity shares at a premium of rs.

Shares are quoted at rs. 22 on the date of allotment of bonus shares. Give journal entries to record the above transaction. I the declaration of bonus at the rate of rs.

I the declaration of bonus at the rate of rs. Give journal entries to record the above transaction. 22 on the date of allotment of bonus shares.

Shares are quoted at rs. 12 00 000 and this bonus is to be paid by issue of fully paid equity shares at a premium of rs. The company declared bonus out of its reserve fund of rs.

Following journal entries are required to account for a bonus issue. Bonus issue is a simple reclassification of reserves which causes an increase in the share capital of the company on one hand and an equal decrease in other reserves.